July 10, 2026

Why Chasing the Wrong Numbers Can Cost You Money

Discover why impressive financial metrics can mislead investors. Learn the behavioural finance principle that helps you identify real value and avoid costly mistakes

Read more

Bank fixed deposits have been the traditional, go-to option for Indian investors for over three decades. However, FD interest rates currently fall between 4-5%, far less than the returns offered by mutual funds.

Naturally, there arises a need for an investment option that's just as safe as an FD but offers similar or better returns. Enter, liquid mutual funds.

In this blog, we'll take a look at the difference between liquid funds and how it compares to traditional bank FDs in terms of returns, liquidity, safety, and availability of options.

Banks lend money to borrowers with the capital individuals invest in fixed deposits, savings accounts, and recurring deposits. That's why banks pay you interest in exchange for staying locked-in in FDs.

Liquid funds are debt funds that invest in relatively safe securities like T-bills, commercial paper, corporate bonds, government bonds, and more. “Invest” means to lend money when it comes to debt funds.

“Invest”, in the context of debt funds, means that the fund lends money to the government, corporations, etc. The fund receives an interest in exchange which is the returns that investors earn. This is what makes them safer than other mutual funds. You can consult a Cube Wealth Coach or download the Cube Wealth App.

Bank FDs carry a lock-in period of 7 days to 5 years. Your money will be blocked in the FD throughout the tenure and there are penalties for premature withdrawals. However, partial withdrawals are allowed during emergencies. This is good for overtly conservative folks and those who are not aware of better financial instruments.

Liquid mutual funds, on the other hand, do not carry a lock-in period and are highly liquid. Liquid fund withdrawals are generally processed in 1-3 business days which can be very useful for emergencies.

Though the returns on Liquid Mutual Funds are not guaranteed. Did You Know? The Cube ATM feature allows you to withdraw money from your liquid fund investment to your savings account in less than 30 minutes.

Gone are the days when FD returns were as high as 13%. Currently, the interest rate on bank FDs ranges from 4-5% which is generally lower than the returns generated by the best liquid funds on the Cube Wealth app.

Truth be told, bank FDs are one of the safest investment options available to Indian investors. FDs are not linked to the market and don't lose their value during volatile economic conditions.

Moreover, FD returns are guaranteed. On the other hand, liquid funds are known to be safer than other mutual funds. The portfolio of a liquid fund matures in 60-91 days.

This simply means that the liquid fund gets its principal back within 60-91 days while generating reasonable returns through the interest earned.

It's important to remember that liquid funds are market-linked instruments that are riskier than FDs. But, here's the important upside, liquid funds are unlikely to erode your wealth as they grow with the market.

Read this blog to know more about the best SIP mutual funds in India

The purpose of investing in FDs could include generating stable returns with relatively high safety and availing tax benefits. However, you must evaluate the following factors before investing in FDs. You can consult a Cube Wealth Coach or download the Cube Wealth App.

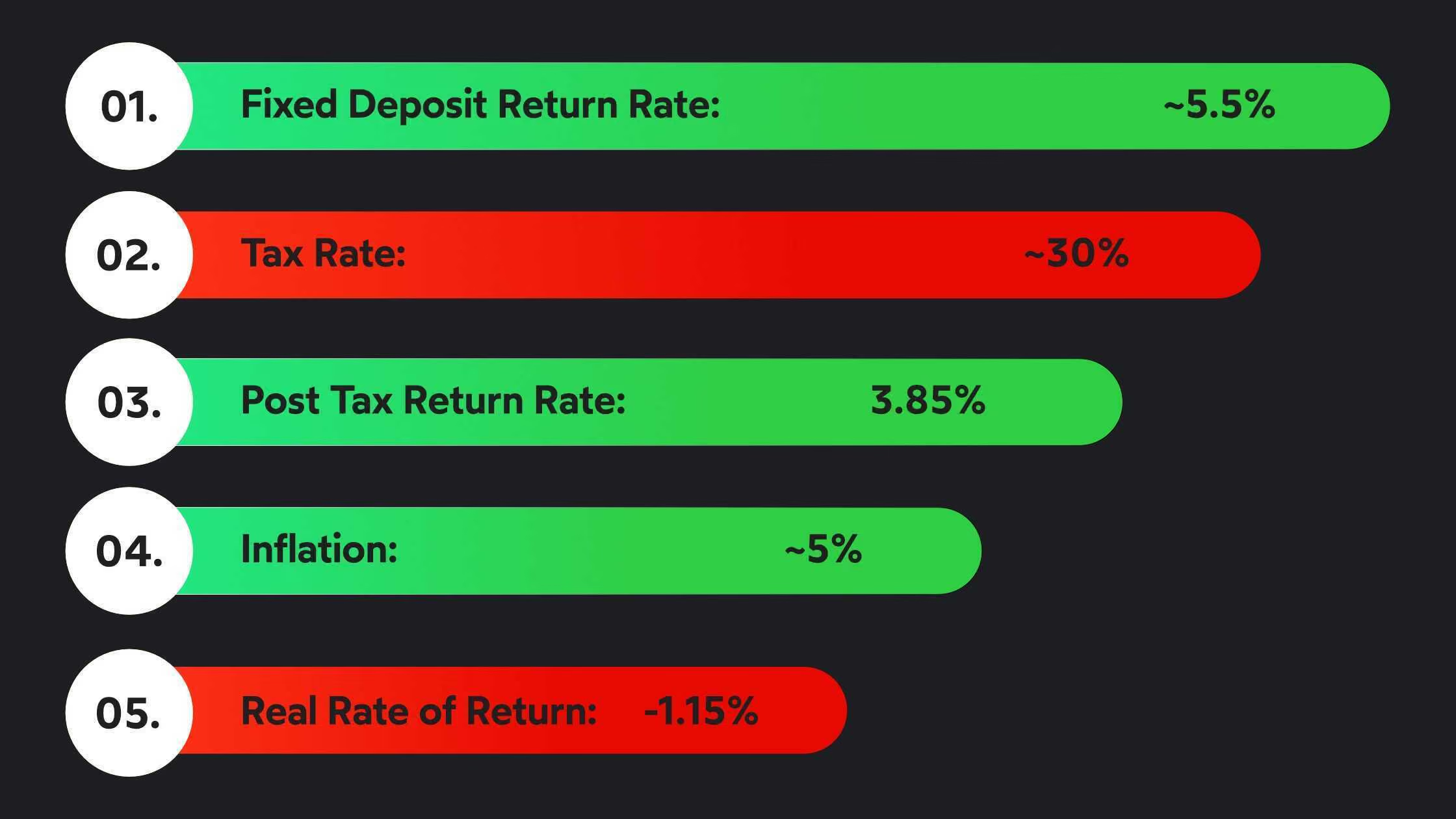

There's no way around it - bank FD returns have been plummeting since the early 1990s. However, the appeal of FDs lies in the fact that they are known to be safe and can generate 4-5% returns.

You must evaluate if these returns, along with the relative safety, can be useful to your portfolio for diversification or as a means to rebalance an aggressive or moderate portfolio.

Read this blog to know more about investment options better than FDs

Not all FDs can help you save tax. In fact, almost all FDs fall under this umbrella except one - tax-saving FDs. These FDs can help you claim deductions of up to ₹1,50,000 under Section 80C.

Here's the catch - the lock-in tenure is 5 years and the interest earned (>₹40,000) is taxable. Tax benefits aside, the returns earned through FDs have been known to barely beat inflation on top of being taxed.

The purpose of investing in liquid funds broadly includes having access to high liquidity for short term financial goals, emergencies, or as a pitstop for Systematic Transfer Plans (STPs).

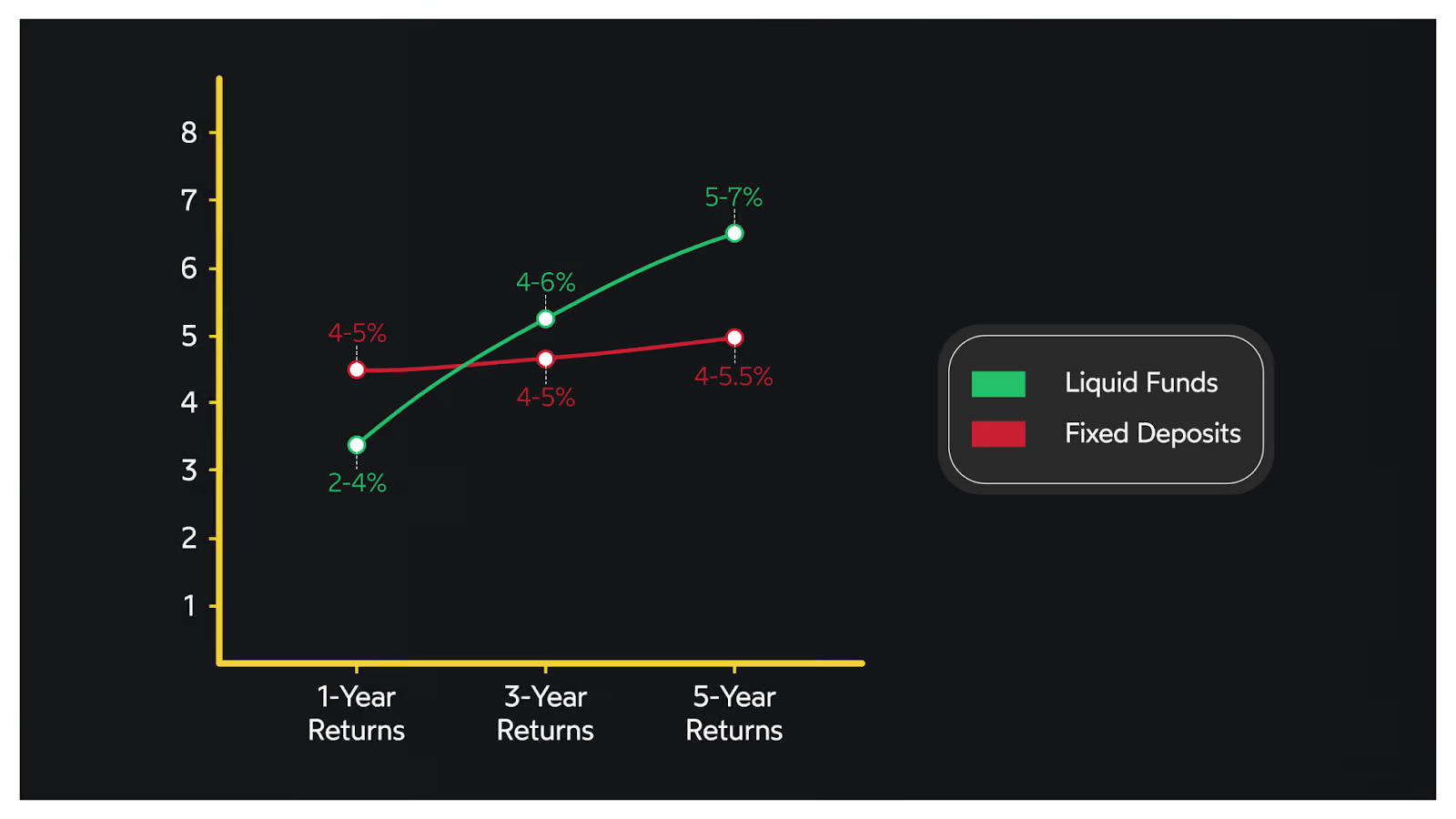

Historical data suggests that liquid mutual funds generate returns in the 5 to 7% range. They invest in debt securities and their portfolio matures relatively quickly.

That's why liquid funds are suitable for the short term and emergency bucket. That does not however mean that liquid funds are not ideal for the medium term. Here's a comparison of liquid fund returns Vs FDs.

Liquid funds are taxed like debt funds. The taxation looks like this:

The purpose of FDs and liquid mutual funds are different. However, the returns generated by FDs barely beat inflation. That's the trade-off - high safety with the dwindling returns and strict lock-in periods.

Conversely, liquid funds are known to generate better returns than FDs over 3+ years with better liquidity. Moreover, liquid funds offer an indexation benefit where the purchase price is adjusted to reflect inflation.

Liquid mutual funds vs FDs is a tough debate. But liquid funds have a clear edge over FDs when it comes to:

At the end of the day, what you should invest in will depend on the portfolio that you want to build and the wealth creation goals that you have in mind.

Even if you decide liquid funds are great for your portfolio based on a risk analysis quiz or a call with a Cube Wealth Coach, the conundrum doesn't end there.

Liquid funds are a thriving category of mutual funds with too many scheme options to choose from. But wait, there's a solution. Cube simplifies this for you to make the investment journey easier.

Cube's mutual fund advisor, Wealth First, helps you cut through the noise by selecting a handful of the top liquid funds in India. Here's how you can invest in these top-performing liquid mutual funds:

2. Complete eKYC

3. Take risk quiz

4. Get curated liquid funds

5. Start investing

Ready to roll? Get started now

Watch this video to know more about handpicked mutual funds on Cube WealthFAQs

Ans. Fixed deposits are a traditional investment option where an individual deposits a lump sum amount with a financial institution or bank for a specified tenure at a fixed interest rate. They are known for capital preservation and guaranteed returns.

Ans. Liquid funds are market-linked mutual funds that invest in short-term debt instruments, offering the potential for higher returns but with some market risk. Fixed deposits, on the other hand, provide guaranteed returns and are not market-linked. FDs offer capital protection and a fixed interest rate.

Ans. Liquid funds are generally considered better for short-term cash management because they provide higher liquidity and have the potential for better returns than fixed deposits. However, the choice depends on individual financial goals and risk tolerance.

Ans. Taxation varies between liquid funds and fixed deposits. Interest earned on fixed deposits is subject to income tax, while gains from liquid funds are taxed as capital gains, which can have different tax rates based on the investment duration.

The choice between liquid funds and fixed deposits depends on your specific financial objectives, risk tolerance, and liquidity needs. Each option has its advantages and considerations.

Liquid funds are a suitable choice for short-term cash management, offering high liquidity and the potential for better returns compared to fixed deposits. They are market-linked mutual funds, which means returns can vary based on market conditions. However, they are still relatively low risk compared to other mutual fund categories. You can consult a Cube Wealth Coach or download the Cube Wealth App.

Fixed deposits are known for their capital protection and guaranteed returns, making them a preferred choice for risk-averse investors. They provide a fixed interest rate and offer stable returns, making them ideal for individuals seeking income certainty and capital preservation.

Other Posts You May Like:

Schedule a call based on your convenience. And get an expert to help you invest.

.png)

The financial life game that makes learning fun!

Let's get in touch

Want the best

investment blog delivered straight to your inbox?

Grow your money without wasting time

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!