July 10, 2026

Why Chasing the Wrong Numbers Can Cost You Money

Discover why impressive financial metrics can mislead investors. Learn the behavioural finance principle that helps you identify real value and avoid costly mistakes

Read more

If you’re an Indian investor, you’d know that the words “safe” and “predictable” are synonymous with one of India’s favourite investment options, the traditional bank fixed deposit.

But is a fixed deposit enough for your wealth to actually grow over time, beat inflation, and help you achieve financial freedom? Sadly, no!

That can only happen if the asset outperforms inflation by generating reasonably high returns. These are traits that modern bank FDs don’t possess.

Fixed deposit returns barely beat inflation and at best, lie between the 4-5% range. However, FDs are still popular and trusted by many Indian investors.

But why? It would help to understand the historical context of FDs to answer this question. You can consult a Cube Wealth coach or Download the Cube Wealth app.

In the 1980s, RBI had given banks the freedom to set their own interest rates for FDs (up to 8%) that matured in a year. This limit was pushed to 13% in the 1990s for FDs that matured after 46 days.

Imagine having the option to invest in such a safe yet lucrative financial instrument in the 1990s. After all, 13% is a relatively high interest rate even today. However, something changed in the early 2000s.

FD interest rates fell to an all-time low below 5%. At the same time, market-linked instruments like stocks and mutual funds began to gain prominence as they generated relatively high returns and liquidity.

This also explains why the older generation trusts and loves FDs - they really were a solid option back in the day. Today, however, they pale in comparison to even the most average of mutual funds and stocks.

The classic bank FD works in a straightforward way. Banks lend money to borrowers and they need capital for that. They get access to the required capital by tapping into your fixed deposit.

That’s why FDs carry a lock-in period that ranges from a few weeks to years. The bank pays you interest in exchange for your investments, that’s the return that you earn which ranges from 4.5-5.5%.

Senior Citizens FDs work the same way as regular FDs. However, there’s one important difference. Fixed-term deposit interest rates are higher for senior citizens by as much as 0.5% as opposed to regular citizens. You can consult a Cube Wealth coach or Download the Cube Wealth app.

A tax-saving fixed deposit can help you claim deductions of up to ₹1,50,000 under Section 80C. But there’s a catch. Tax saving FDs carry a lock-in period of 5 years. Average returns may range from 4.5 to 5.5%.

A Flexi Fixed Deposit is a combination of a savings/current account and a fixed deposit. It basically allows you to access the high liquidity of a savings account and the predictable fixed deposit returns.

Corporate FDs are offered by NBFCs. They’re generally known to offer higher returns than a regular bank fixed deposit. The average returns range from 5.5-6.5%. However, Corporate FDs are considered to not be as safe as bank FDs.

Bank fixed deposits are safe because they are backed by the Deposit Insurance and Credit Guarantee Corporation (DICGC) scheme, which ensures that up to ₹1,00,000 of your capital, including interest, is safe at all times.

The returns generated by a bank FD is predictable and is known before making the investment. While this is true, RBI’s interest rate changes may have an impact on the returns.

FDs are non-market linked options which means that the volatility of the equity market doesn’t have an impact on the returns.

Emergencies may lead to a cash crunch that would require you to access capital immediately. However, you don’t need to liquidate your FD - you can take a loan against the FD that serves as collateral. You can consult a Cube Wealth coach or Download the Cube Wealth app.

There are benefits to investing in FDs as mentioned above. The historical value and the assured returns may appeal to investors with a lower risk appetite.

Truth be told, FDs are safe but at the same time, the returns they generate barely beat inflation and lead to stagnation of wealth. Achieving goals like financial freedom may not be easy in that case.

Whether or not you should invest in FDs would depend on your investment goals and risk appetite. However, there are other assets that outperform inflation by generating reasonably high returns than bank FDs. Read on to know more.

Debt funds are known to be a relatively safe type of mutual fund. They generally invest in AAA/AA+ rated bonds and other debt securities with the aim of generating solid returns in the range of 6-8%.

Liquid mutual funds fall under the debt funds category and carry a relatively lower risk compared to other mutual funds. The low risk does not mean that liquid funds are a pushover.

They can still generate reasonably better returns than a bank FD in the range of 4-6%. Moreover, withdrawing bank FDs can be a tedious process as the conventional way involves a lot of paperwork.

You might also have to factor in the bank executive’s lunchtime break. However, liquid funds are far easier to redeem. The withdrawals are processed in 3-5 business days, all online.

Your withdrawals can be transferred straight into your bank account in less than 30 minutes if you use Cube ATM. Learn more about it here.

Large-cap funds invest in reliable, trusted, and iconic companies that are industry leaders in their own right. They fall under the equity funds category and are known to generate 10-12% returns on average.

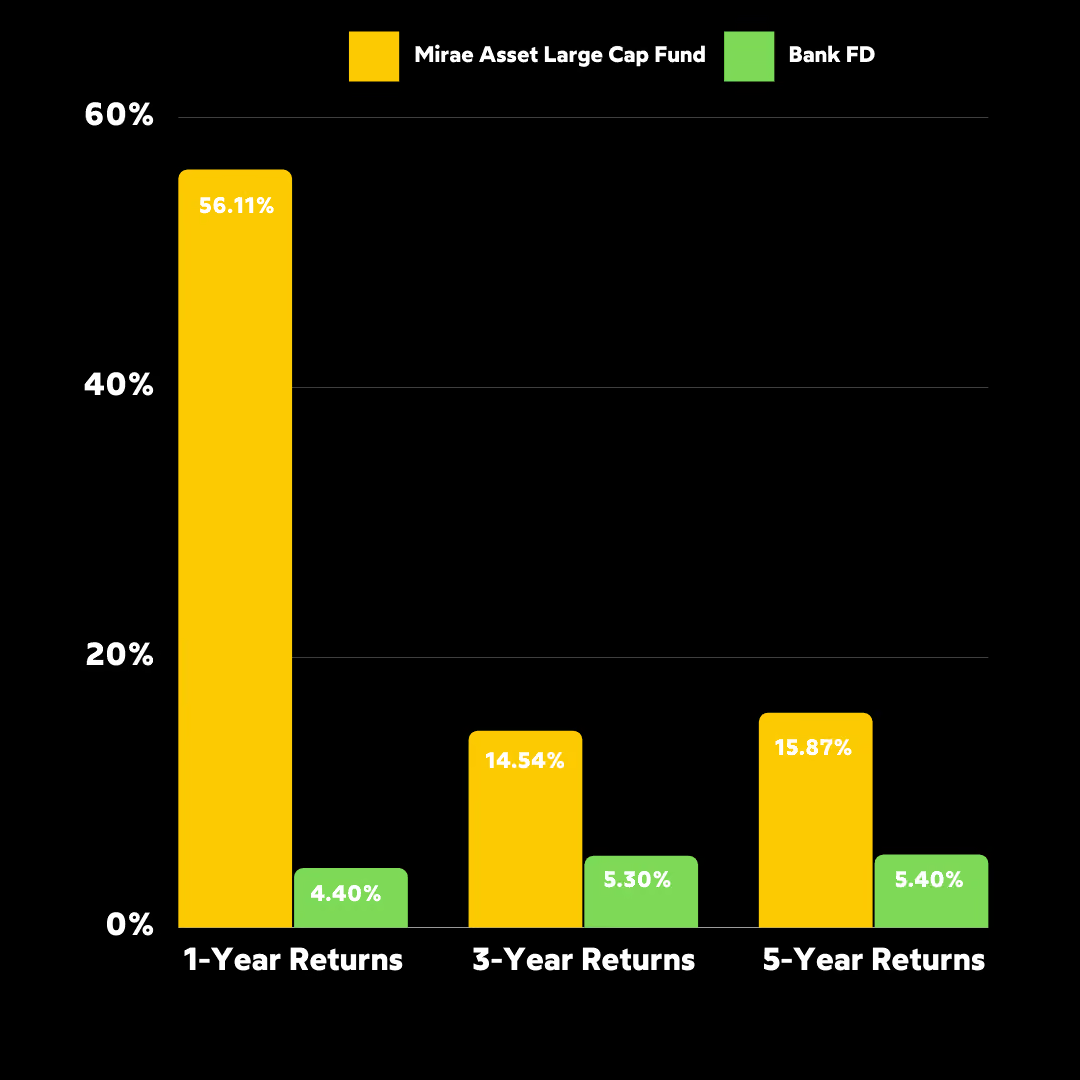

Investing in large-cap funds over FDs has two benefits. One, your investment grows with the market that gives it a better chance to outperform inflation. Two, the returns are almost 2-3x that of FDs.

For example, let’s compare the returns of a top mutual fund on the Cube Wealth app, Mirae Asset Large Cap Fund versus a bank FD.

Point to note, large-cap mutual funds carry a higher risk than debt funds, liquid funds, and bank FDs. However, they’re known to be far more stable than other equity funds.

It would be wise to invest in large-cap funds based on your risk appetite. Take Cube’s Free Risk Analysis Quiz to understand your risk level and get recommended investment options from reliable advisors.

P2P lending on Cube Wealth allows you to become a lender who loans money to borrowers with RBI Certified P2P Lending NBFCs, Faircent and LiquiLoans. FDs and P2P lending have two things in common:

However, the similarities end there as P2P lending On Cube is an attractive asset class that can generate 8-9.5% returns. Furthermore, P2P lending is a passive income source with recurring payouts.

Cube gives you access to risk-based investment options and thoroughly vetted borrowers. Explore P2P lending on Cube

Asset leasing by Grip on Cube Wealth allows you to become a co-investor in physical assets like cars, furniture, equipment, and more. It is a source of passive income that has benefits over FDs like:

Ans. A bank Fixed Deposit (FD) is a financial instrument where investors deposit a lump sum of money with a bank for a fixed tenure at a predetermined interest rate.

Ans. Bank FD interest rates are determined by the Reserve Bank of India (RBI) and vary according to market conditions and the bank's policies. Longer tenures and higher deposit amounts generally fetch higher interest rates.

Ans. Yes, investors can select the tenure that suits their financial goals, ranging from a few months to several years, depending on the bank's terms.

Ans. Bank FDs are preferred for their safety and stability. They offer a guaranteed return and are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) for up to Rs. 5 lakh per account.

Bank fixed deposits are safe, reliable, and non-market linked instruments that once generated high returns. However, things have changed over the past few decades.

Investing in FDs may not be optimal when compared with other investments like debt funds, liquid funds, large-cap funds, P2P lending, and asset leasing. The reason behind this is twofold.

To start with, FDs have been known to fall short when it comes to outperforming inflation. This can lead to a stagnation of wealth which can stunt or hold back your portfolio.

Furthermore, bank fixed deposit rates fall in the low range of 4.5-5.5%. For context, it would take approximately 6.5 years for a ₹1,00,000 investment to compound into ₹2,00,000 if you invest in an asset with 12% returns.

It would take the same ₹1,00,000 more than 11 to 12 years to compound into ₹2,00,000 if you invest in a bank FD with 5.5% interest. Explore Best Alternatives To FDs

Watch this video to know more about the best ways to invest your money

Schedule a call based on your convenience. And get an expert to help you invest.

.png)

The financial life game that makes learning fun!

Let's get in touch

Want the best

investment blog delivered straight to your inbox?

Grow your money without wasting time

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!