July 10, 2026

Why Chasing the Wrong Numbers Can Cost You Money

Discover why impressive financial metrics can mislead investors. Learn the behavioural finance principle that helps you identify real value and avoid costly mistakes

Read more

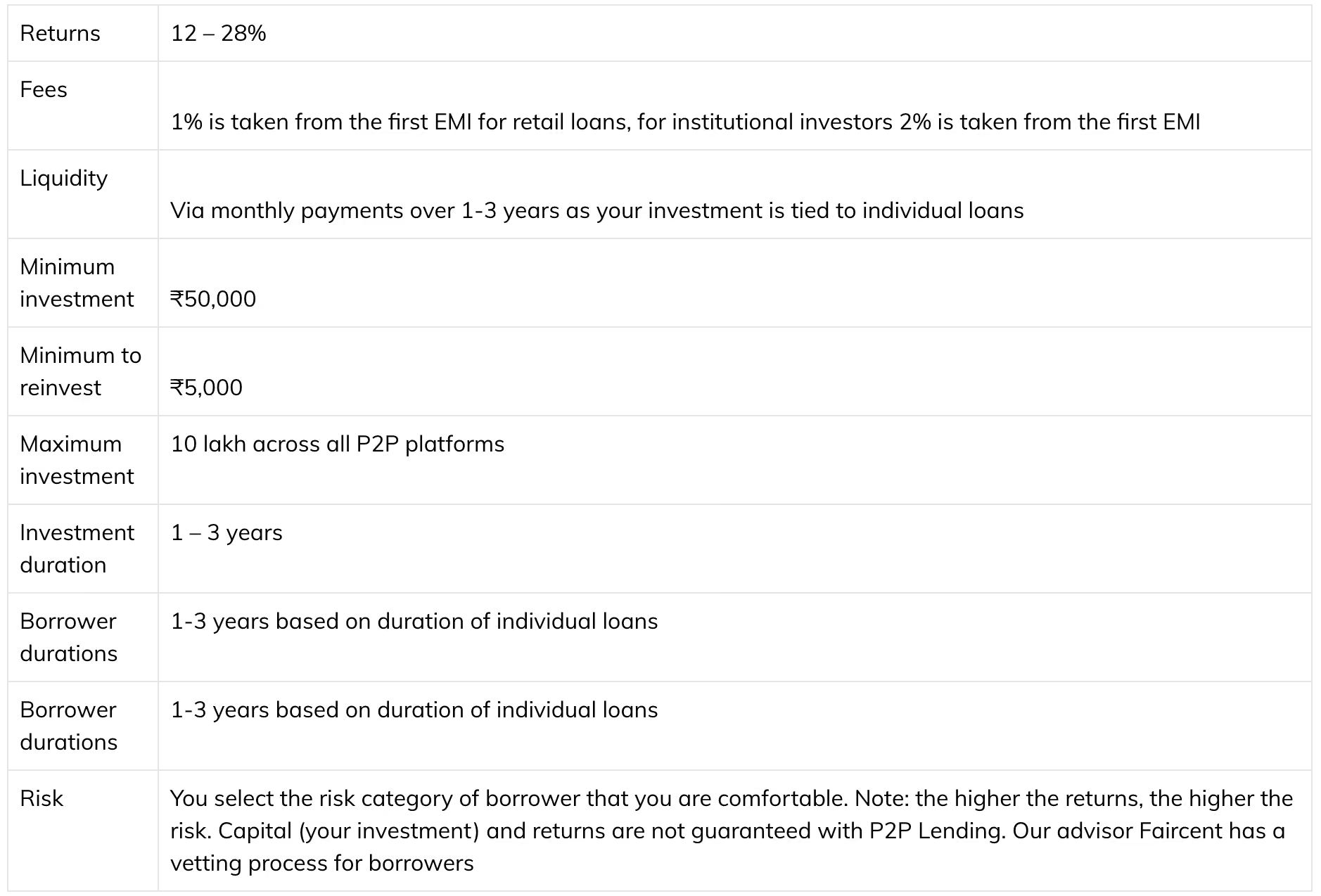

Learn how to earn 12-28% returns simply by creating your very own lending portfolio where you don't even have to vet the borrowers.

P2P is short for peer to peer. Simply put - you become the bank. Banks lend your money out and keep a percentage of the profits for themselves. With P2P you remove the middleman (the bank) so that you can earn more. This type of P2P lending is direct to the borrower however you are using a specialist platform that uses technology to make this process safe and efficient instead of having to do all of the administration yourself. You can consult a Cube Wealth coach or download the Cube Wealth App.

P2P commenced in India in 2012 and is forecast to be a $5 billion industry by 2023.

Use P2P to diversify the medium and high risk components of your portfolio for short term returns over 1-3 years. It’s also good for boosting monthly cash flow.

● No upfront fees. Faircent (Cube’s P2P advisor) only earns when you earn your first monthly EMI payments from borrowers.

● You receive principal and interest payments each month for the duration of each of the loans you fund which boosts monthly cash flow.

● Auto reinvest your monthly borrower payments.

● Great returns 12-28% based on your risk preference.

● You can’t withdraw your investment in one lumpsum because your investment has been allocated to a loan for an agreed period of time.

● A buyer could default and if recovery collection were to be unsuccessful, you could lose part or all of your initial investment for that particular loan.

Faircent Founded in 2013 and named in the prestigious ‘Super Start Ups 2017’ list by Superbrands. Faircent were the first to be certified by the RBI as an NBFC- P2P. Faircent has over 5,600 lenders and disbursed over INR 40 crore as loans to borrowers. Faircent are industry leaders when it comes to P2P in India.

Faircent's innovation and credibility is what made them the standout P2P Advisor for us at Cube Wealth. We all had great experiences testing Faircent with our own personal investments. We were able to build a unique experience for our Cube Wealth Investors where they simply select the P2P risk category they are comfortable with and the amount they want to invest. Everything else is done for the investor!

Cube Wealth members don't need to worry about selecting the borrowers or the amount they want to loan them. So this really is the simplest way to set up your own P2P lending portfolio. Transparent portfolio tracking and our SuperSIP feature makes monthly reinvesting easy. You can consult a Cube Wealth coach or download the Cube Wealth App.

Faircent enables lending and borrowing to suitably vetted parties without having to go through a traditional financial intermediary like a bank. As an investor, your investment is pooled with other investors then allocated to multiple borrowers to minimise risk. For example, you may loan to 30-60 borrowers for a Rs. 50,000 investment. Borrowers are credit worthy and assigned a risk profile following Faircent assessment.

All investors (lenders) and borrowers must be KYC’d to meet compliance requirements. Faircent have a strict selection criteria for vetting borrowers that looks at their personal, professional and financial details and authenticate it. As Faircent approves a borrower they assign a risk rating and loan interest rate. They then match borrowers to lenders that have selected that borrower risk category.

A contract is created and the loan is dispersed. Borrowers make periodic payments on both the principle and the loan as an EMI payment. Faircent also engages a professional collections agency process to assist in recovering loans where a borrower has defaulted. Based on risk class, the default rate is 4-6%.

Investor funds are moved from their bank account to an escrow account and held until they are dispersed to borrowers. Repayments are also made back into the escrow account the with borrower EMIs. You can consult a Cube Wealth coach or download the Cube Wealth App.

P2P is an investment worth adding to your portfolio for great returns with diversification outside of the market.

Ans. P2P lending platforms facilitate the process. Borrowers create loan listings, and investors can choose to fund a portion or all of the loan. Once fully funded, borrowers receive the loan, and investors earn interest.

Ans. Interest rates are typically determined by the P2P platform or may be set through a bidding process where borrowers request loans at specific interest rates, and investors choose to fund them at their preferred rates.

Ans. Regulations governing P2P lending vary by country and region. Some areas have established regulatory frameworks to ensure the safety and transparency of P2P lending platforms.

Ans. Yes, P2P lending can generate passive income as investors earn interest on their loans. However, it requires active management and due diligence in selecting loans.

Peer-to-peer (P2P) lending presents an innovative and accessible avenue for both borrowers and investors to meet their financial needs. P2P lending platforms have reshaped the traditional lending landscape by connecting individuals directly, often resulting in more favorable loan terms and investment opportunities. While the industry offers potential benefits, such as higher returns for investors and easier access to credit for borrowers, it's not without risks. Evaluating the credibility of P2P platforms, diversifying investments, and conducting due diligence are essential practices for both lenders and borrowers. As this sector continues to evolve, staying informed about the latest regulations and industry developments is crucial for anyone considering P2P lending as part of their financial strategy.

Other Posts You May Like:

Schedule a call based on your convenience. And get an expert to help you invest.

.png)

The financial life game that makes learning fun!

Let's get in touch

Want the best

investment blog delivered straight to your inbox?

Grow your money without wasting time

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!