July 4, 2025

7 Common Investment Mistakes And How To Avoid Them

Avoid these 7 common mutual fund mistakes Indian professionals are making in 2025. Learn how to invest smartly with SIPs and avoid panic selling. Start here.

Read more

“Most people overestimate what they can do in 5 years, and underestimate what they can do in 15.” — Bill Gates

I’ve seen this play out in investing again and again.

A 32-year-old earning ₹30L wants to retire by 40.

A 45-year-old with ₹5 crore still doesn’t feel secure enough to slow down.

That gap—between what we think financial freedom looks like and what it actually takes—is exactly where the FIRE movement sits.

Let’s unpack it properly. No fluff.

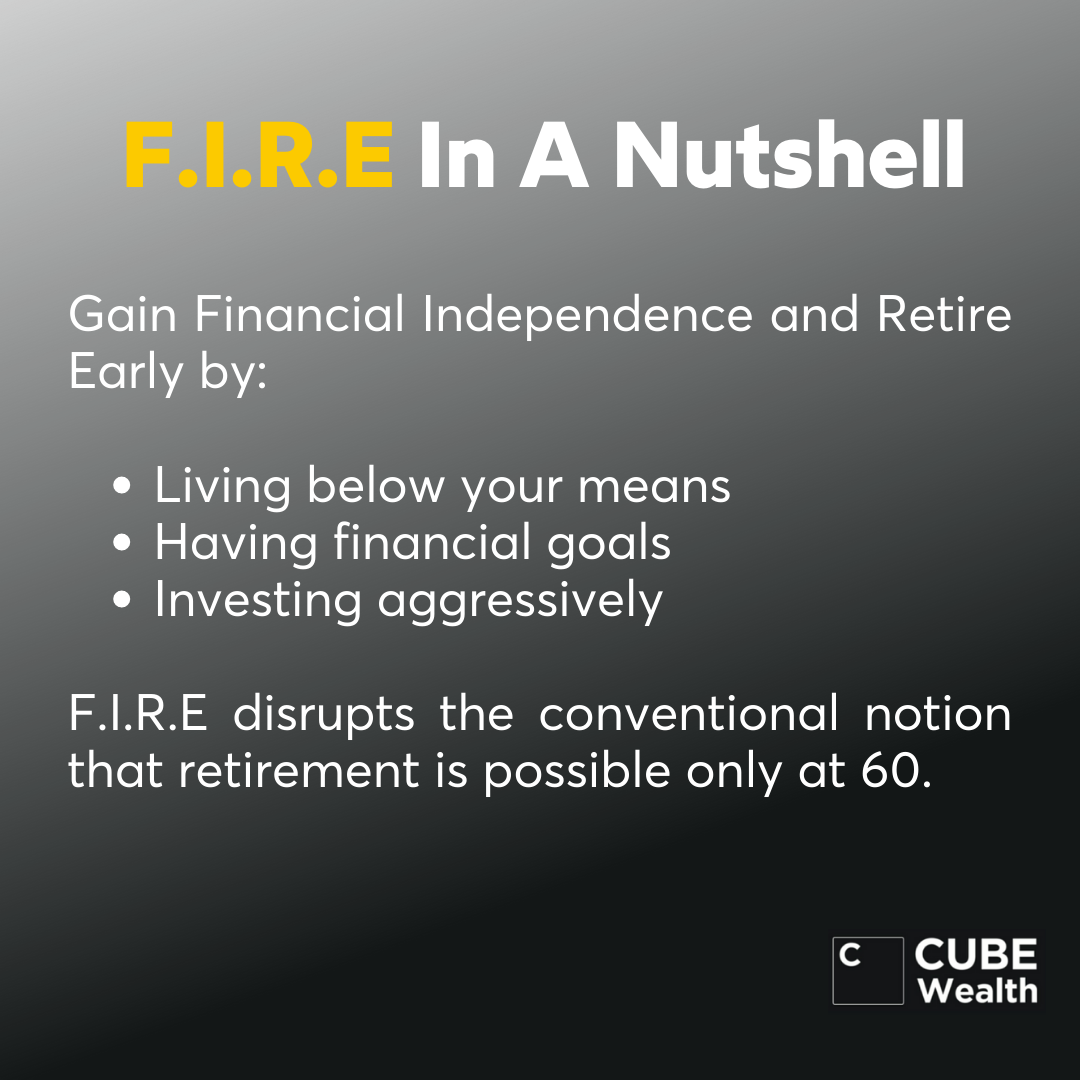

FIRE—Financial Independence, Retire Early—is often misunderstood.

It’s not about quitting your job at 35 and moving to Goa.

It’s about reaching a point where:

Your investments can fund your life, whether you choose to work or not.

That’s a very different goal.

In India, where most people grew up with the idea of working till 58–60, this shift is huge. But also confusing.

Because the question isn’t:

“Can you retire early?”

The real question is:

“Can your money sustain your lifestyle without a salary?”

At the core of FIRE is a simple calculation:

FIRE Corpus=25×Annual Expenses\text{FIRE Corpus} = 25 \times \text{Annual Expenses}FIRE Corpus=25×Annual Expenses

Let’s make this real.

If you spend ₹1.5 lakh a month in a city like Bangalore or Mumbai:

Now pause.

Most people focus on returns.

Very few get this part right—their actual lifestyle cost.

And that’s where FIRE plans quietly fail.

It’s not random.

I see three clear shifts:

A decade ago, ₹15L salary felt like “sorted”.

Today? It barely feels enough in Tier 1 cities.

Rent. Travel. Dining. Upgrades.

Every raise comes with a bigger life.

FIRE forces a hard question:

Are you upgrading your life faster than your wealth?

Earlier, long hours meant ambition.

Now, people are asking:

What’s the point if I can’t step off this treadmill?

FIRE offers that exit. Or at least the possibility of one.

You no longer need a broker or insider access.

Today you can build a serious portfolio with:

Execution is easy now.

Discipline? Still hard.

Let’s keep this practical.

You keep expenses very low. Almost aggressively.

This works on paper. In reality? Tough.

I’ve rarely seen someone sustain this in Mumbai or Bangalore without feeling restricted after a few years.

This is what most urban professionals think they want.

But here’s the trade-off:

You’re not retiring early. You’re just retiring comfortably.

And that usually takes time.

This is the most practical version I see working.

You build a decent corpus. Not massive.

Then you switch to:

Your investments cover a big chunk. Your income fills the rest.

Less pressure. More control.

You invest aggressively early.

Then you stop chasing growth and just let compounding do its job.

You still work. But you’re not dependent on saving aggressively anymore.

This works beautifully if you start in your 20s.

Let’s cut through the theory. Here’s what works.

Skipping coffee won’t get you to FIRE.

This will:

Moving from 20% to 40% savings rate is powerful.

Moving from 40% to 50%? Marginal.

This is where most FIRE content gets it wrong.

You don’t reach financial independence by cutting expenses alone.

You get there faster by:

A ₹5L income jump beats ₹5,000 saved any day.

A typical FIRE portfolio today looks like:

Why?

Because inflation in India—especially lifestyle inflation—is real.

If your portfolio grows at 7–8%, and your life costs grow at 6–7%, you’re barely moving ahead.

Markets fall. News gets noisy.

People panic.

They stop SIPs. Exit early. Wait for “better timing”.

And that breaks the entire FIRE journey.

Wealth creation isn’t about brilliance.

It’s about not interrupting compounding.

This is the part people skip.

Which is why I rarely recommend “pure FIRE”.

A more practical approach is:

Flexible FIRE — where you have options, not rigid timelines.

Let’s not romanticise this.

Yes. But probably not the way Instagram shows it.

Very few people will:

But many can:

That’s a big shift.

Don’t chase early retirement.

Chase financial flexibility.

Because the real win isn’t quitting work.

It’s being able to say:

“I don’t have to do this anymore.”

And still choosing to.

Nevertheless, it’s important to aim for financial freedom if not F.I.R.E. Step #1 to become financially independent is to speak to a wealth coach to make your hard-earned money work for you.

Read this blog to know how a Cube user is achieving financial freedom.

Watch this video to know how busy professionals can grow rich

F.I.R.E stands for 'Financial Independence, Retire Early'. The goal of the movement is to invest aggressively when young to retire in your 30s or 40s (before the traditional retirement age).

F.I.R.E or Financial Independence, Retire Early is a movement that focuses on investing aggressively in your 20s, 30s, and 40s (50-75% of your income) to retire early (in your 40s or 50s).

There are 4 popular types of F.I.R.E movements that vary in degree of investing & end goal:

The FIRE number is the amount of money an individual or household needs to maintain their desired lifestyle without working. It's calculated by estimating annual expenses and multiplying them by a factor, typically 25-30, which represents the expected withdrawal rate from investments.

The FIRE movement may not be suitable for everyone, as it requires strict financial discipline and a willingness to make significant lifestyle adjustments. It's important to assess one's own financial goals and comfort level with the principles of FIRE before committing to the lifestyle.

Challenges of FIRE may include healthcare costs, market volatility, and the need to maintain a frugal lifestyle for an extended period. Unforeseen financial emergencies could also disrupt early retirement plans.

Top 5 Reasons To Try Our Powerful Investment App!

Schedule a call based on your convenience. And get an expert to help you invest.

Let's get in touch

Want the best

investment blog delivered straight to your inbox?

Grow your money without wasting time

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!