FIRE in India (2026): The Truth About Retiring Early — And What Actually Works

Can you actually retire early in India? Discover the math, the mindset, and the investment strategies needed to reach financial independence without the fluff.

1. Incomes Have Gone Up. So Has Lifestyle Pressure.

A decade ago, ₹15L salary felt like “sorted”.

Today? It barely feels enough in Tier 1 cities.

Rent. Travel. Dining. Upgrades. Every raise comes with a bigger life.

FIRE forces a hard question: Are you upgrading your life faster than your wealth?

2. Burnout Is No Longer a Badge of Honour

Earlier, long hours meant ambition.

Now, people are asking: What’s the point if I can’t step off this treadmill?

FIRE offers that exit. Or at least the possibility of one.

3. Investing Has Become Accessible (Finally)

You no longer need a broker or insider access.

Today you can build a serious portfolio with:

Direct mutual funds

Global equities

Bonds and fixed income

Structured products

Execution is easy now.

Discipline? Still hard.

The 4 Versions of FIRE (And What Actually Works in India)

Let’s keep this practical.

Lean FIRE — The Minimalist Route

You keep expenses very low. Almost aggressively.

This works on paper. In reality? Tough.

I’ve rarely seen someone sustain this in Mumbai or Bangalore without feeling restricted after a few years.

Fat FIRE — The Comfortable Route

This is what most urban professionals think they want.

No lifestyle compromise

Premium living

Large corpus (₹8–15 crore or more)

But here’s the trade-off:

You’re not retiring early. You’re just retiring comfortably.

And that usually takes time.

Barista FIRE — The Realistic Middle Ground

This is the most practical version I see working.

You build a decent corpus. Not massive. Then you switch to:

Consulting

Freelancing

Part-time work

Your investments cover a big chunk. Your income fills the rest.

Less pressure. More control.

Coast FIRE — The Quiet Strategy

You invest aggressively early.

Then you stop chasing growth and just let compounding do its job.

You still work. But you’re not dependent on saving aggressively anymore.

This works beautifully if you start in your 20s.

How to Actually Build FIRE (Without Burning Out)

Let’s cut through the theory. Here’s what works.

1. Fix Your Savings Rate — But Don’t Obsess Over Small Cuts

Skipping coffee won’t get you to FIRE.

This will:

Keeping rent < 25–30% of income

Avoiding unnecessary EMIs

Not upgrading your lifestyle after every hike

Moving from 20% to 40% savings rate is powerful.

Moving from 40% to 50%? Marginal.

2. Focus on Income First. Always.

This is where most FIRE content gets it wrong.

You don’t reach financial independence by cutting expenses alone.

You get there faster by:

Switching jobs strategically

Building a second income stream

Negotiating better compensation

A ₹5L income jump beats ₹5,000 saved any day.

3. Invest for Growth, Not Comfort

A typical FIRE portfolio today looks like:

60–70% equity (mutual funds + stocks)

10–20% international exposure

10–20% debt

Why?

Because inflation in India—especially lifestyle inflation—is real.

If your portfolio grows at 7–8%, and your life costs grow at 6–7%, you’re barely moving ahead.

4. Stay Invested. This Is Where Most People Fail.

Markets fall. News gets noisy.

People panic.

They stop SIPs. Exit early. Wait for “better timing”.

And that breaks the entire FIRE journey.

Wealth creation isn’t about brilliance.

It’s about not interrupting compounding.

5. Plan for What Can Go Wrong

This is the part people skip.

Health costs

Family responsibilities

Career breaks

Market downturns

Which is why I rarely recommend “pure FIRE”.

A more practical approach is:

Flexible FIRE — where you have options, not rigid timelines.

The Honest Pros and Cons

Let’s not romanticise this.

What Works

You gain control over your time

Financial stress reduces significantly

You build strong money habits early

What Doesn’t

Extreme frugality can backfire

Retiring too early can feel directionless

Indian realities (family, healthcare) add pressure

So… Can You Really Retire Early in India?

Yes. But probably not the way Instagram shows it.

Very few people will:

Retire at 35

Never earn again

Live purely off investments forever

But many can:

Become financially independent by 40–45

Take career breaks without stress

Choose work instead of needing it

That’s a big shift.

A Better Way to Think About FIRE

Don’t chase early retirement.

Chase financial flexibility.

Because the real win isn’t quitting work.

It’s being able to say:

“I don’t have to do this anymore.”

And still choosing to.

Nevertheless, it’s important to aim for financial freedom if not F.I.R.E. Step #1 to become financially independent is to speak to a wealth coach to make your hard-earned money work for you.

Watch this video to know how busy professionals can grow rich

FAQs

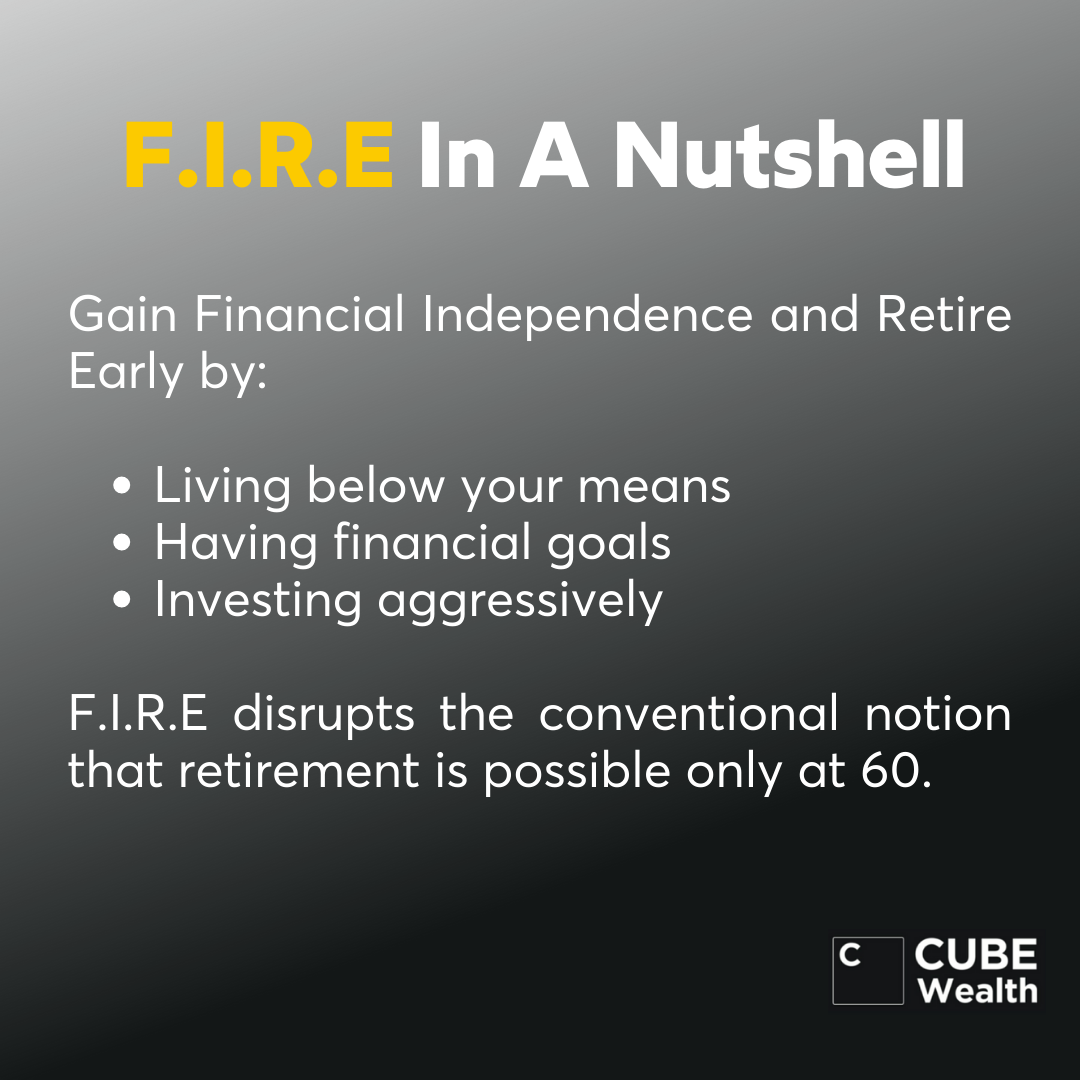

1.What does FIRE movement stand for?

F.I.R.E stands for 'Financial Independence, Retire Early'. The goal of the movement is to invest aggressively when young to retire in your 30s or 40s (before the traditional retirement age).

2. How does the FIRE movement work?

F.I.R.E or Financial Independence, Retire Early is a movement that focuses on investing aggressively in your 20s, 30s, and 40s (50-75% of your income) to retire early (in your 40s or 50s).

There are 4 popular types of F.I.R.E movements that vary in degree of investing & end goal:

Lean F.I.R.E

Fat F.I.R.E

Barista F.I.R.E

Coast F.I.R.E

3. How does one calculate their FIRE number?

The FIRE number is the amount of money an individual or household needs to maintain their desired lifestyle without working. It's calculated by estimating annual expenses and multiplying them by a factor, typically 25-30, which represents the expected withdrawal rate from investments.

4. Is the FIRE movement for everyone?

The FIRE movement may not be suitable for everyone, as it requires strict financial discipline and a willingness to make significant lifestyle adjustments. It's important to assess one's own financial goals and comfort level with the principles of FIRE before committing to the lifestyle.

5. What are some potential challenges associated with FIRE?

Challenges of FIRE may include healthcare costs, market volatility, and the need to maintain a frugal lifestyle for an extended period. Unforeseen financial emergencies could also disrupt early retirement plans.

Barun is an experienced wealth management professional with over 13 years of expertise in guiding individuals and institutions on their investment journeys. He possesses a deep understanding of financial markets, encompassing a wide range of products, including mutual funds, stock advisory, complex structured products, forex, bonds, and corporate NCDs. He is NISM VA and XXI A certified, as well as IRDAI certified for insurance.

Share this story on:

Top 5 Reasons To Try Our Powerful Investment App!

Schedule a call based on your convenience. And get an expert to help you invest.

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!

Thanks For Subscribing!

We'll send you interesting emails about exciting investment options.

Oops! Something went wrong while submitting the form.

Upload your mutual fund statement for tailored recommendations and a comprehensive portfolio review.

Upload Your Consolidated Account Statement from CAMS

We'll email your personalised mutual fund review in a few days—our experts, who have 40+ years of experience, go beyond quick algorithms to deliver deep, customised insights.

To get recommendations aligned with your goals, fill out your risk profile here.

For any questions, feel free to reach us at wealth@bankoncube.com

How to Download Your Consolidated Account Statement (CAS)